This research insight is divided into 4 parts where

we have accentuated the comparison between the macro factors over the last 9

years, followed by the new DII, the impact of the U.S slowdown, and finally the

interest rate increase impact on the equity market. These 4 parts will help to

get clarity on our market expectations and outlook. There is

too much lack of clarity and constant comparison of the market with the last 10 years

in order to get clarity on the direction of the market. It's nothing but

confusion and lack of clarity that is guiding the investors and not the market.

You are still expecting Nifty to be around 15000

levels but I am sorry to disappoint you that NIFTY will surprise you with new

highs over the next 6 months. The prime problem of not being able to believe

this is that we are comparing Indian markets with the past 10 years' market

pattern and not data. If we look at the data we will find significant enough

rationales to find and understand the new Indian economy and market. If

we look at the macro factors comparison between 2013 and current we find huge

differences in the strength and maturing of the current Indian economy.

Well, the increase in the number of tax filing and growth in govt revenue plays

a critical role for the Indian equity market to grow more aggressively in

coming years. It also proves the strength of the market too.

We have witnessed FII’s redemption to the

tune of Rs.2.6 lakhs cr resulting market to fall 16% from 18500 levels to 15200

levels and that’s too for continuous 8 to 9 months. If we look at the

historical redemption pattern of FII’s outflow and market fall we will find

that NIFTY should have been at 10000 levels and we should have entered the bear

market phase. But we stopped at 15200 and we rebounded from that levels back to

18000 levels within the last couple of months. The reason being the DII’s

market has transformed significantly in the last decade. The DII’s market

is so strongly matured that we are no longer much dependent on FII’s money.

Many of the readers will disagree but I accept the same with an open mind.

The above data clearly throws light on the transformation and strength of the DIIs and the maturity of the inflows. This is the major part we missed while doing the market outlook and mistake in calculating that the market will fall to 13000 to 14000 levels. Another segment we missed out on while calculating the market direction is that currently we have a significant number of new Demat account holders who are first-time investors and they risk takers and investing with a long-term vision in the market.

Indian market is moving significantly from the

traditional mode of investments in physical assets to financial assets. Total

Household Assets as of date is Rs.802 lakh cr and Equity in total Household

assets is Rs 39lakhs cr which is just 4.8%. We dig deep we find that 4.8%

comes to 2.52 lakhs cr in the Equity market and out of that current annual SIP

book size of India is Rs.1.44 lakhs cr. Hence a long scope of investment in the

equity market is yet to be explored which supports the DII’s market compared to

FII’s market. This scope also reduces our dependency on FIIs and more on DIIs.

Coming to the macro front we find that India has only a crude problem and that too has been resolved through a strategic tie-up with Russia and other countries for crude supply. Further, as the International crude prices fall we will be getting more lower prices from Russia and other countries which helps India in every term.

This will be a hidden significant

boost for the Indian markets. Monsoon, Festive season, Rural demand, and

all triggers are present every time, every year in the market, what we need to

know is how the next 5 years the market will change over in its earnings,

demand, and opportunity for the market. The corporate profit-to-GDP ratio

attains an 11-year high of 4.3% in FY22 and this is going to increase in the

coming years as the Indian business ecosystem takes a significant turnaround.

The recent example of the 5G and EV market is just a small step towards a

revolution across ancillary sectors.

Coming to U.S Recession well every slowdown shifts

inflows to emerging economies once the optimum level of the slowdown is faced.

Further interest rate falls down begins once the optimum level is reached.

Hence in both ways, the Indian market will get inflows. If we look at the

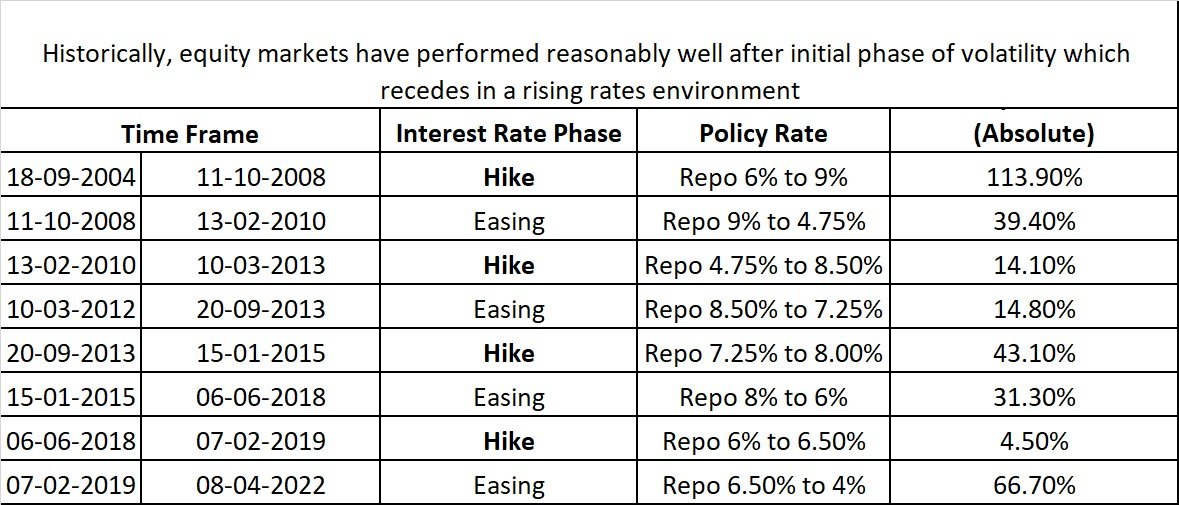

interest rate cycles and their impact analysis on the market well I am sorry to

disappoint you that in every case investing in equities was the best option and

decision taken by investors historically.

Hence from the above charts, it is well clear that even if interest rates go

hike Indian equity market will not be giving negative returns. More importantly

within these 18 years' time frame, you have witnessed many wars and many global

events not favoring the market, etc but still, the market gave a return to the

investors. This proves that the concept of market timing is a big myth

& the notional loss of not investing is huge.

The current macro speaks strongly that the Indian market is far different from the global market and this is the place where we are having problems in building trust in Indian equities to reach new highs when the developed economy is struggling. The change in supply chain and change in demand has transformed the market for India. Hence stop daydreaming for Nifty to 13000 levels and invest in equities with a long-term vision.

0 Comments:

Post a Comment