The Indian markets till now have attracted significant inflows from FPI’s. For them the Indian market is stable and has significant room for growth. FPIs sold a cumulative amount of Rs 60,000 crore in January, April, and May but bought Rs 63,200 crore in February, March, and June together. On the debt side they have invested to Rs 77,109 crore this year so far. Why FPI’s is buying and from where the inflows are coming? Is their going to be any change in the FPI’s inflows in coming days?

Will this Best Bull run of the market will continue? How long

FPI’s will invest in India? Well, the article has tried to accentuate to its

bets effort but one must read the conclusion of the same. Coming back the DII’s don’t need any more clarification about the

quantum of investments being done by them. Mutual fund has become one of the

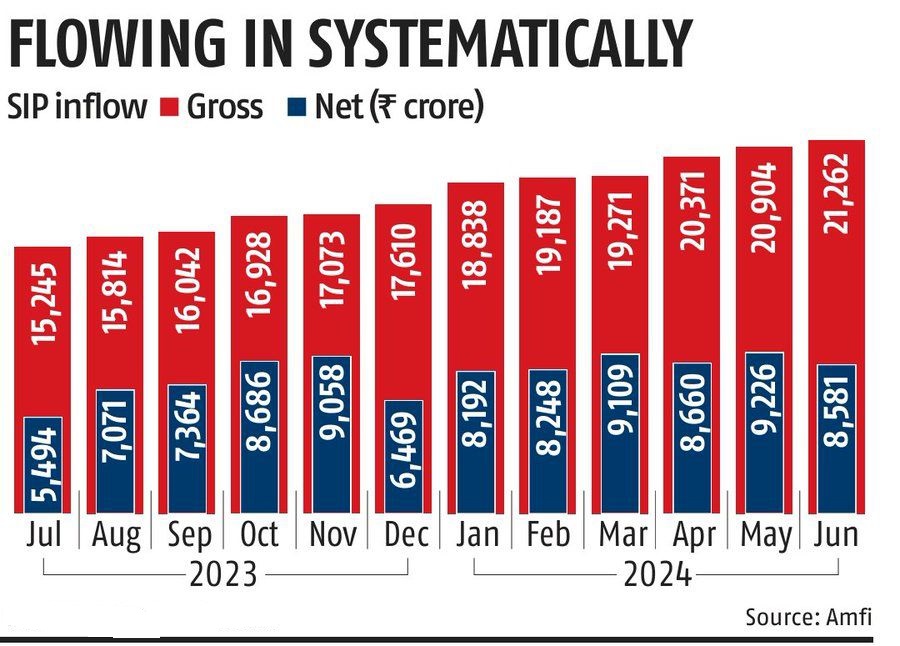

strongest contribution of inflows into the market. If we look at the SIP route

we find the following analysis:

·

April to June 2024: Gross SIP inflows

increased steadily from April (20,371 Cr) to June (21,262 Cr), indicating

consistent investor participation and confidence in mutual fund investments

over the quarter.

·

April to June 2023: Gross SIP inflows in the

corresponding period of 2023 were lower overall, with April (13,728 Cr), May

(14,750 Cr), and June (14,735 Cr), reflecting a notable increase year-over-year

in 2024.

Net SIP Inflows

·

April to June 2024: Net SIP inflows for the

quarter totaled 26,467 Cr, calculated as gross SIP inflows minus outflows from

redemptions and switches. This figure indicates the actual net investment

flowing into mutual funds after considering withdrawals.

·

April to June 2023: Net SIP inflows in 2023

for the same period were 18,281 Cr, showing a substantial increase in net

investments in 2024, highlighting growing investor confidence despite market

fluctuations.

Net to Gross Ratio

·

April to June 2024: The net to gross ratio

for SIP inflows averaged at 42% over the quarter, with slight variations

month-on-month (April: 43%, May: 44%, June: 40%). This metric reflects the

proportion of net investments relative to total gross investments.

·

April to June 2023: In contrast, the net to

gross ratio in 2023 was slightly higher, averaging 42%, suggesting a comparable

efficiency in converting gross investments into net inflows despite lower gross

numbers.

So its well clear and even the net SIP

numbers are quite high for the market inflows from the DII’s perspective.

FPI's Portfolio Attraction Increases India Allocation

The long-only portfolio focusing on India, launched on July 1, 2021, has demonstrated robust performance over recent quarters, outperforming key benchmarks and reflecting strong investor confidence. In the last quarter, the portfolio recorded a significant 16% increase in US dollar terms on a total-return basis. In comparison, the MSCI India benchmark posted a gain of 10.4% during the same period. Year to date, the portfolio has continued to excel, achieving a notable rise of 31.6%, surpassing the benchmark's 17.1% gain by a considerable margin as of the end of the second quarter of 2024.

.jpg)

The portfolio's overarching strategy remains anchored in leveraging India's long-term domestic demand dynamics. This focus not only aligns with broader economic growth trends but also positions the portfolio favorably amidst evolving market conditions.

When

the same comparison is drawn with China portfolio its being found that the

China long-only portfolio, launched on September 3, 2020, demonstrated strong

performance in the last quarter, achieving an 8.5% increase in US dollar terms

on a total-return basis. In comparison, the broader market as represented by

the MSCI China Index rose by 7.2%, while the CSI 300 Index experienced a slight

decline of 1.5% during the same period.

Get ready for more inflows from FPI’s provided there is no sudden hiccups

from the government budget and other policy reform measures. Several

adjustments were implemented in the Asia Pacific ex-Japan relative-return

portfolio, primarily in response to notable shifts in neutral weightings. These

changes were made with the aim of aligning the portfolio more closely with the

new Asia Maxima strategy.

Specifically, the

weighting allocated to India was increased by 1.5 percentage points,

maintaining a slight overweight position compared to the benchmark. Where as China & Hong Kong were reduced by one percentage point and half of a percentage

point, respectively. This proves well how FPI’s treat Indian market and what

type of inflows will come to us.

But this does not mean that one should sell all his property and do investments in equity market. Don’t be so much blind and even be guided by greedy financial advisor. One should follow his asset allocation rules and risk profile. Please do remember that since 2020 Indian markets have not seen any major correction like the historic ones. Hence once correction might change the dynamics of the market for short term. Those who are gambling in the market taking risk against all assets should immediately avoid such practices and should adopt to its core asset allocation principles. Rebalancing should be part of wealth management. Those who are leveraging assets to invest in equity markets should be very careful and should take this as word of caution. The market favours the fortune who are for long term.

.jpg)

0 Comments:

Post a Comment