This article is in continuation to the 1st series written way back 4 months before. Investing has become a nightmare when the market is hovering at 18600 and every day the market is making new highs. Investors have lost 25% return from the levels of 15200 to till date predicting that markets (NIFTY) will come down to the level of 12000. We forget that this India is driven by a different breed of investors who do0 not carry the legacy of Harshad Mehta, and Ketan Parekh. In simple words, these investors are not grey hair investors. In the last 2 and half years India has added 2.5 cr of New Investors through Demat. We need to know who is investing and who is having the money to deploy in the markets and how much we are dependent on FIIs.

Online broking has changed the broking and the base of the client has also changed dramatically. From students to Housewives everyone is now active in trading. Thanks to Youtube and all those masters in the broking Industry who came up with online courses on the stock market and technical courses to upgrade and uplift the knowledge base of the clients. Hence the client base is no longer restricted to a certain class of investors. The broader participation of the investors and society has changed the meaning of DII. The direct ownership of retail investors has increased by 110 bps to 9.5% compared to the pre-pandemic levels.

Thanks to all the MFDs and the NDs who played vital roles in getting the Mutual Fund Industry to be a size of 40lakh cr industry where Equity went up from 1.8 lakhs cr in 2012 to 16 lakhs Cr by 2022. Today’s Investors know the benefit of rupee cost averaging and know the NAV Journey of Reliance Growth Fund from Rs.32 in 2004 to the current nave of Rs2100. In fact, today investors also do SIP in Direct equity stock which has changed the dynamics of Equity investing and also the client behaviour towards Equity.

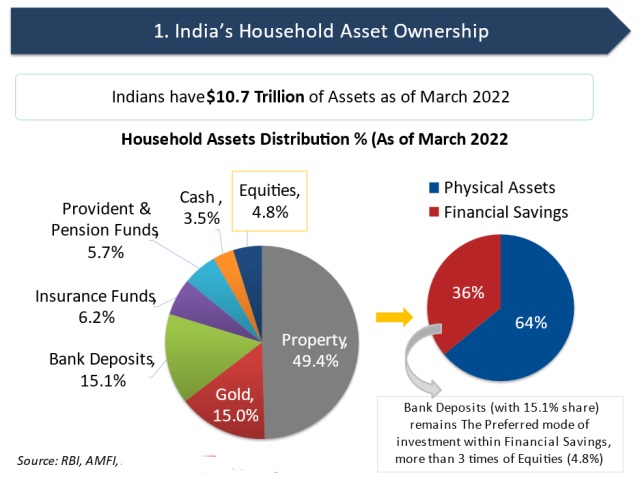

As the per capita Income of India keeps raising the investments into financial assets also go up improving much higher allocation into Equity. Today Equity Investments stand around 4.8% of the total 804 lakh cr of Household assets of India. Retired people are also becoming more active participants in trading since they have enough time and significant savings to play beyond safe products where returns are below 6%.

If we look at the markets we find that the NSE-listed companies' market cap has become 4X in the last 15 years. CDSL and NSDL both combined have added up 34.3 million registrations in the previous year whereas the total number of Depositories crosses above 100 million. The New startup culture has breaded new investors with significant cash flows followed by ESOPs. Real estate is no longer an asset class to look for investing and with PAN becoming mandatory the equity market is the only left-out option.

As the Indian economy travels towards the journey of US$ 5 trillion mark savings and investing will grow up both. Further, these investors who are going to the part of the Indian GDP of 5 trillion marks are risk takers and hence the flow into equities will rise. Retail investors’ participation is increasing and being a young population the risk-taking ability pushed up the market married with knowledge about rupee cost averaging in falling markets.

MFDs have played a pivotal role in this 40 lakhs cr Indian Mutual Fund market. In my 18 years of career, I have seen very closely the transformation of the MFDs and their mode of operating business. From a Post of MIS agent to becoming a 1000 cr AUM-based, MFD is a big journey travelled by this community. Financial advisory models have taken dramatic change and today’s MFDs are all highly knowledgeable which gives a significant shape and guidance to the investors resulting in investment flow change dramatically. The young breed of MFDs is highly technology driven and hence it matches the frequency of the investors who are tech-savvy.

Market timing has become a myth now. It’s no longer having a practical impact while investing in the long term. 10 years before today’s NIFTY was Sensex and tomorrow's NIFTY will be the Sensex of today.

.jpg)

.jpg)

.jpg)